.jpg)

The aviation industry faces increasing pressure to achieve meaningful decarbonization and corporate net-zero goals. While intended to provide guidelines in this transition, the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) presents airlines with additional challenges.

For many, the primary challenge of CORSIA is finding a way to mere compliance: 67 percent of respondents in a survey by PwC and IETA expect an undersupply of eligible credits by 2027. However, there is not just a looming shortage of eligible carbon credits, but a severe lack of high-quality credits approved for meeting CORSIA obligations.

This shortage presents airlines with a crucial decision: simply meet the minimum compliance requirements, or use this opportunity to demonstrate true climate leadership. This article examines the complexities of CORSIA, including how airlines can leverage it to integrate high-integrity climate action into their core business strategy.

The aviation sector’s decarbonization challenge

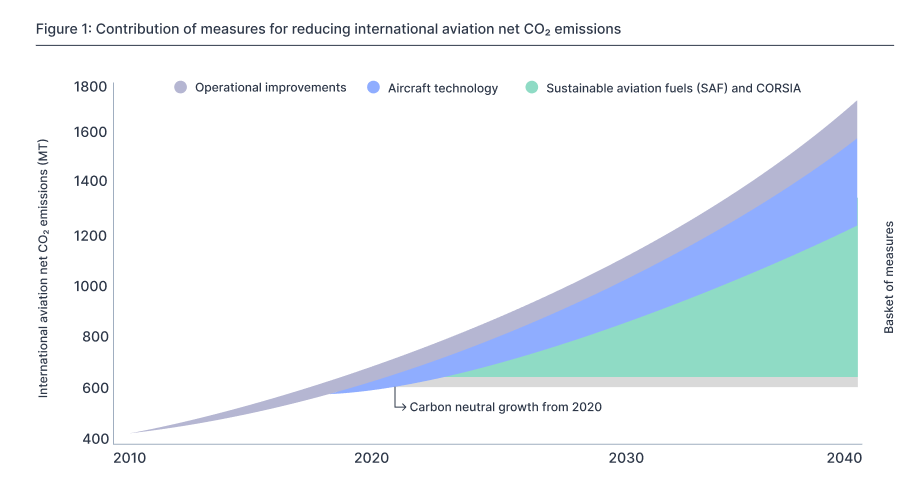

Aviation contributes about 2.5 percent of global CO2 emissions, a figure expected to grow as passenger traffic is forecasted to double by 2050. Even as other industries decarbonize, aviation is considered “hard to abate.”

Unlike ground transport, long-haul flights cannot be electrified in the near future. While sustainable aviation fuels (SAFs) are a key solution, their availability is minimal (less than one percent of global jet fuel consumption), and costs remain prohibitively high compared to conventional jet fuel. This mismatch between industry growth and decarbonization capabilities makes a standardized mitigation strategy imperative.

One solution to this challenge comes in the form of sustainable aviation fuel certificates (SAFc) or CORSIA-approved carbon credits, which can be combined into one multi-asset portfolio through partners like CEEZER to help CORSIA-compliant companies effectively decarbonize.

What is CORSIA?

Administered by the International Civil Aviation Organisation (ICAO), CORSIA is the industry's plan for “carbon-neutral growth,” capping net CO2 emissions at 85 percent of 2019 (pre-COVID) levels. Airlines from participating states must compensate any further emissions by purchasing and retiring Eligible Emissions Units (EEUs)—approved carbon credits—or deploying CORSIA-eligible fuel types (e.g., SAFs). Demand for credits is projected to be substantial, estimated at 150-250 million credits annually by 2035.

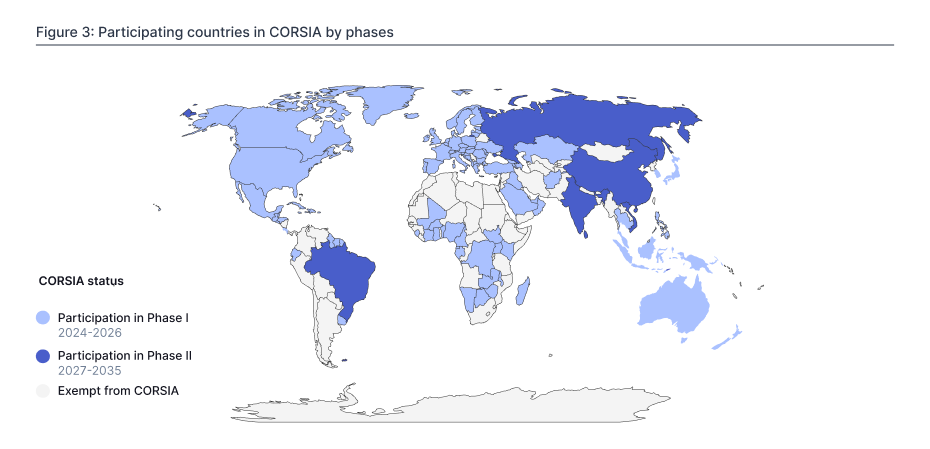

CORSIA is rolling out across three phases. The Pilot Phase (2021-2023) had negligible demand due to suppressed air travel during the COVID pandemic. All eyes are now on the Phase I (2024-2026), which requires airlines from ICAO member states, voluntarily participating in the Phase I, to monitor and report emissions and compensate for them by January 2028.

The mandatory Phase II (2027-2035) will encompass nearly all ICAO members, with limited exceptions. This expansion, bringing in major aviation states like China, India, and Brazil that did not join the initial voluntary phases, is expected to raise the scheme's coverage from approximately 64 percent to nearly 87 percent of international aviation emissions. However, enforcement mechanisms vary widely. While some states have clearly defined fines, such as the UK's £100 per tCO2 penalty and Brazil's BRL 50 per tCO2 fine, the specific penalty structures for other major jurisdictions remain absent, including the United States and Canada.

What carbon credits classify as Eligible Emissions Units (EEUs)?

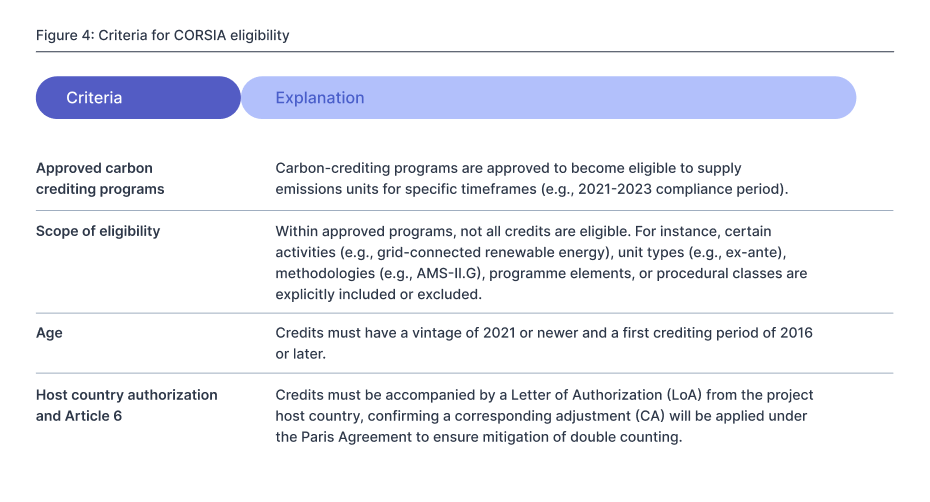

CORSIA’s Technical Advisory Body (TAB) determines the criteria for credits to qualify as EEUs. To be eligible, credits must meet a range of conditions pertaining to the carbon-crediting program, methodology, project type, age, and authorization under Article 6 of the Paris Agreement.

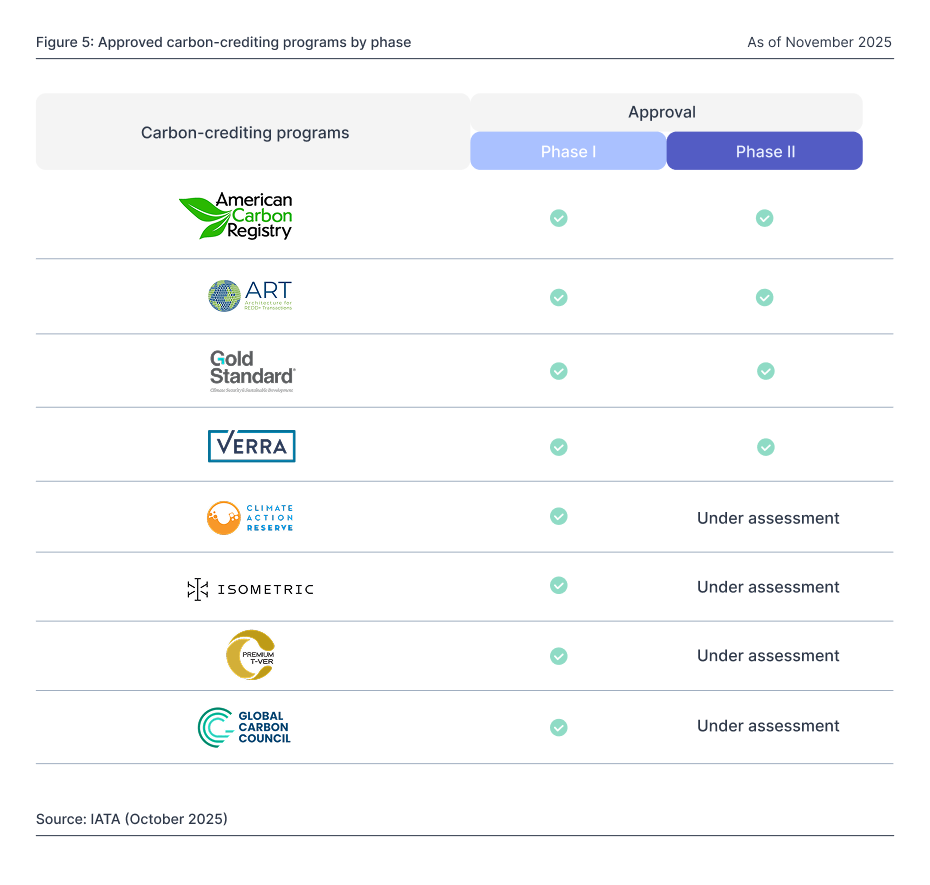

As of November 2025, ICAO has approved eight programs for CORSIA's Phase I and four for Phase II. The TAB will continue assessing three other programs (BioCarbon Fund, FCPF, Global Carbon Council) through March 2026 and will review the Paris Agreement Crediting Mechanism (PACM) once operational. Additionally, ICAO will open a new call for applications in early 2026 for the 2027-2029 compliance period.

However, the linchpin of CORSIA eligibility is host-country authorization under Article 6 of the Paris Agreement, which prevents double claiming by requiring corresponding adjustments. This means if a credit from any nation state is sold to an airline for CORSIA, this country must add one ton CO₂e back to its national emissions ledger. In doing so, the host country gives up its "claim" to that emission reduction, allowing the airline to use it for CORSIA compliance instead.

Crucially, CORSIA only accepts credits carrying a host Letter of Authorization (LoA) that binds the country to make a corresponding adjustment in line with Article 6.2—hence each reduction or removal is used exactly once. While the rules are clear, supply is thin. As of 2025, Guyana’s ART TREES REDD+ project and a cookstoves project in Malawi under Gold Standard are the only projects to issue credits with full CORSIA eligibility, having issued a combined 17 million eligible credits. In October 2025, Japan Airlines and All Nippon Airways became the first operators to publicly retire CORSIA-eligible carbon credits of the Guyana project.

Authorizations under Article 6 are the primary bottleneck. Governments have been urged by the International Air Transport Association (IATA) to address this shortage, but institutional progress is slow. Host country accounting (through LoAs and corresponding adjustments) takes time. This supply shortage may be further exacerbated by uncertainty surrounding US-based projects. Two key eligible registries, the American Carbon Registry and Climate Action Reserve, hold predominantly US projects. However, their CORSIA eligibility is uncertain; due to the recent US withdrawal from the Paris Agreement, these projects will lack the necessary LoAs to become eligible.

The looming demand and supply mismatch in the CORSIA market

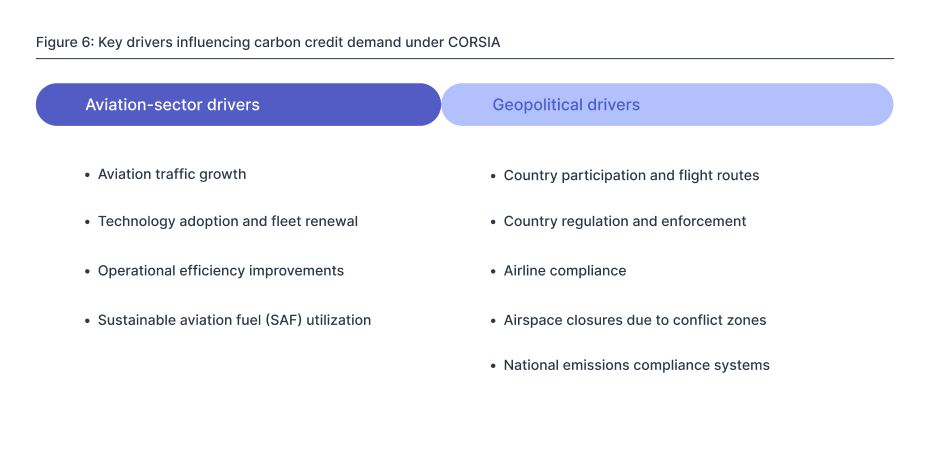

Amongst others, the amount of carbon credits needed by participating airlines is driven by air traffic growth and the expanding list of participating countries.

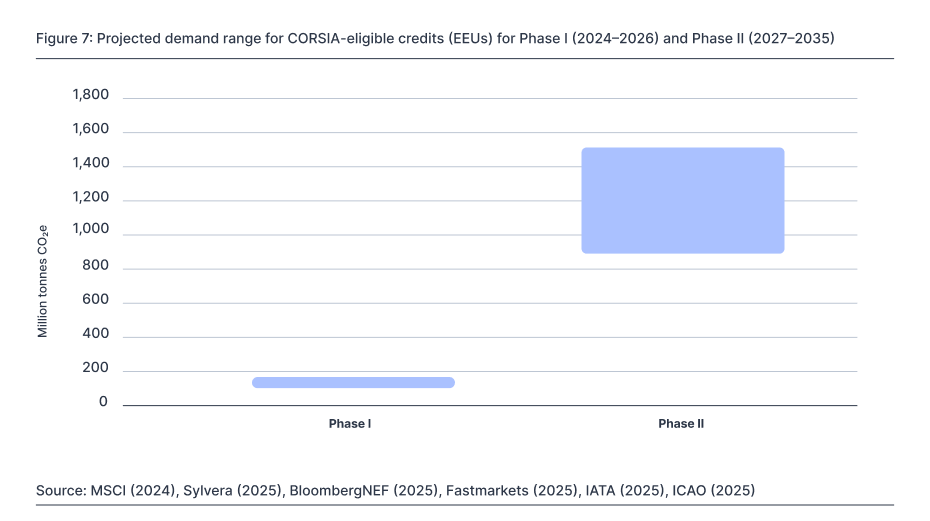

Attempts have been made by various organizations to model this credit demand for Phase I and Phase II. An aggregate view, combining available data, presents the upper and lower bounds of these estimations below.

Even under conservative assumptions, the total demand is expected to reach more than a billion credits — far exceeding the current available supply. This imminent, multi-billion-tonne demand stands in stark contrast to the yet negligible authorized supply of only 17 million eligible credits described above.

Moving from mere projections to real obligations, ICOA provided its first official confirmation of compensation obligations with its Sector's Growth Factor (SGF) for 2024 in November 2025. This translates into a concrete initial demand of 58 million tonnes of CO2e for the first year of Phase I. This demand exceeds the previous estimates illustrated above, reflecting a faster-than-anticipated rebound in air traffic since the COVID-19 pandemic. But even if airlines could find enough credits, they face a second, more insidious problem: quality.

Navigating the quality gap: Beyond the "eligible" label

Even if the supply bottleneck were solved tomorrow, a second issue looms: subpar quality of available credits. Some assume that ICAO's eligibility stamp is a proxy for high environmental integrity. The evidence indicates it may not be.

Independent rating agencies have been blunt. Calyx states that "CORSIA eligibility is not a strong indicator of GHG integrity," noting that a high percentage of eligible projects fall into their lower-quality Tier 2 and 3 categories. Analysis from BeZero confirms this, showing that the pool of "in-scope" credits ranges widely from 'A' (high quality) to 'D' (low quality) and that ”airlines run the risk of procuring credits which have a low likelihood of delivering their carbon claim.”

This presents a serious reputational risk. Airlines will soon face a choice:

- Buy any EEUs available simply to meet compliance, facing a potential public backlash for greenwashing if quality concerns are present (see also Delta Air Lines $1 billion lawsuit over its carbon neutrality claim or lawsuits against Qantas).

- Compete for the tiny sliver of credits that are both high-quality and Article 6-authorized, likely igniting a ferocious price squeeze.

Early CORSIA supply will likely rely heavily on cookstove and community projects, of which many face well-documented overcrediting issues. Luckily, new and improved methodologies, as well as criteria by integrity frameworks like the Core Carbon Principles (CCP), have the potential to improve integrity issues. However, this conservative accounting increases the price and reduces the volume of issuable credits. Because these enhanced integrity measures are not mandatory for CORSIA, many buyers will likely bypass them. Instead, they will likely purchase cheaper, older-vintage credits or credits from projects not adhering to the new standards.

Going beyond compliance: The business case for high-integrity carbon removals

CORSIA compliance is mandatory, but its impact is a choice. Companies can either chase a limited pool of low-cost, potentially risky credits or strategically invest in a portfolio delivering on both compliance and credible climate action.

Let’s get back to the bigger picture first. The aviation sector's own long-term strategy, as outlined by IATA, is clear: the only way to address residual emissions and achieve true net zero is through high-durability carbon removal (CDR). Climate science clearly provides that avoidance credits are only a temporary bridge for hard-to-abate sectors like aviation. IETA calls CDR “critical to offsetting residual aviation emissions that cannot be eliminated by other means,” urging investment in both conventional (forestry, soil carbon) and novel (biochar, BECCS, DAC) approaches. However, considering the like-for-like principle, only novel CDR technologies with sufficient durability will work to neutralize residual emissions.

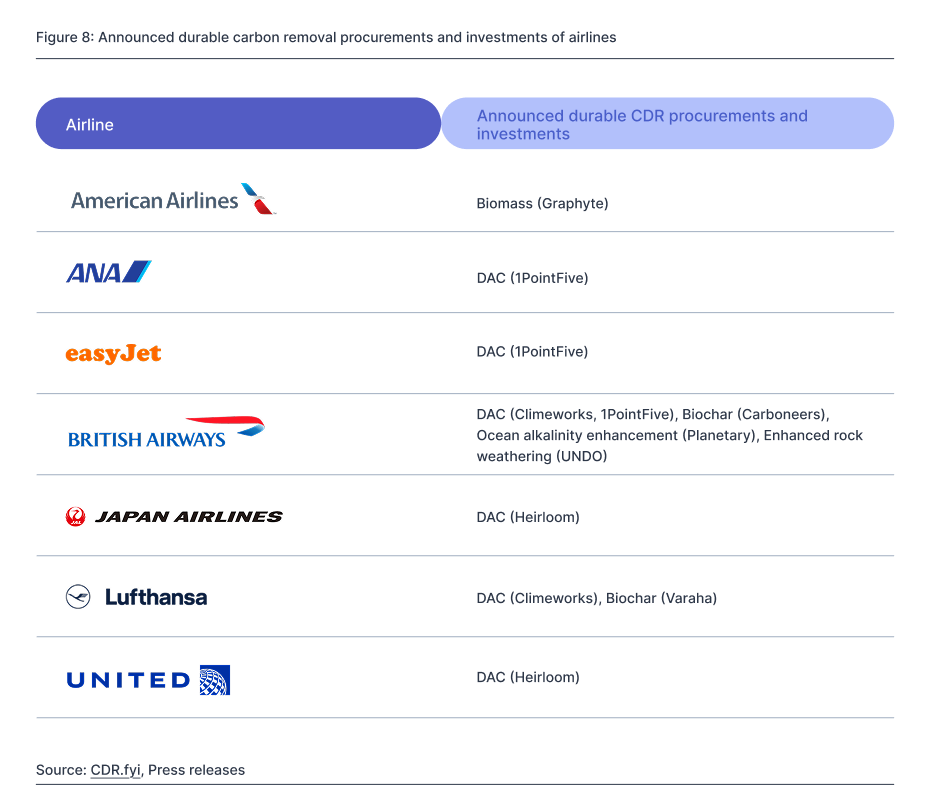

Leading airlines like British Airways, Lufthansa, and United are already partnering with pioneering developers of durable removal projects, signifying the relevance of DAC for neutralization (DACCS) and decarbonization (DAC-to-SAF).

Two things are required for durable CDR to drive aviation's decarbonization: immediate funding and a clear pathway to scale. This is precisely where CORSIA's long-term impact could be most profound.

While CORSIA's current credit pool is dominated by avoidance and reduction credits, its framework is strategically evolving to include high-durability CDR. The Technical Advisory Body (TAB) has already approved Isometric to supply credits for the CORSIA Phase I (2024-2026). For now, the eligibility is limited to biochar (in soils or in construction materials) and direct air capture (stored in saline aquifers or in construction materials).

“The approval by ICAO brings biochar and DACCS into CORSIA for the first time. Isometric's eligibility not only diversifies the supply pool but also provides airlines with access to the most scientifically rigorous and transparent credits on the market to meet their compliance obligations.”

– Lukas May, Chief Commercial Officer at Isometric

“Leading aviation companies are already purchasing our biochar credits via CEEZER, and once these can be used for compliance, we expect many more airlines to follow, driving demand for high-integrity, durable, and cost-effective carbon removals available today.”

– Ikarus Janzen, Co-founder and Chief Commercial Officer at Varaha

In any case, corresponding adjustments under Article 6 of the Paris Agreement will also be a bottleneck for durable CDR that might threaten its inclusion in carbon credit procurement for compliance purposes. This alignment, necessary for CORSIA eligibility, requires host-country LoAs. Not many countries have procedures for inventorization and/or approval systems for novel carbon removal like DACCS or biochar. CEEZER’s due diligence on hundreds of CDR projects reveals that barely any durable projects are close to obtaining LoAs or are even in serious discussions with local authorities to receive them.

“We chose to deploy our DAC project in Kenya because the government is proactively building the policies and Article 6 frameworks needed to issue Letters of Authorization for CORSIA. That clarity gives us the confidence to scale permanent carbon removal here. It also means we can offer airlines a credible way to meet their CORSIA commitments with fully verified carbon removals under the Isometric standard.”

– Thoralf Gutierrez, CEO of Sirona Technologies

In addition, the economic viability of (durable) CDR for CORSIA compliance must be benchmarked against the cost of SAF and SAF certificates (SAFc), which are also eligible compliance pathways under CORSIA Eligible Fuels. Companies adhering to CORSIA can combine these different climate performance assets in one multi-pronged approach to achieve net zero compliantly and effectively, which CEEZER enables through tailored, centralized multi-asset portfolios.

While low-cost reforestation credits ($30–80/tCO2e) are cheaper than all SAF options, high-durability removals like DAC ($600–800/tCO2e) are currently more expensive than the most commercially available SAF using HEFA technology (at $300-600/tCO2e). Both, however, remain significantly cheaper than nascent e-SAF (synthetic jet fuel produced from CO2 captured by DAC) pathways, which are estimated at over $2,300/tCO2e.

In effect, CORSIA can evolve to be a meaningful, lasting demand signal that helps finance and scale CDR technologies the world needs. As Robert Höglund argues, the eligible share of durable CDR could—and arguably should—rise toward 100 percent by 2050.

From obligation to opportunity

With the January 2028 compliance deadline approaching, now is the time for airlines to develop proactive procurement strategies. Real money is already being spent on CORSIA, credits are being retired, and the infrastructure around host country authorization, insurance, and registry integration is maturing. The supply scarcity creates a clear competitive advantage for airlines that act decisively. Locking in access to high-integrity credits now, before that scarcity intensifies, is a smart financial move.

For airlines, the business case for investing in quality credits is clear:

- Future-proof strategy: Building a diversified portfolio that includes durable CDR mitigates reputational and litigation risk and aligns with a credible, science-based climate strategy.

- Enhance credibility: Using high-integrity credits demonstrates a genuine commitment to net zero, building trust with investors, customers, and regulators.

- Drive market transformation: Signaling demand for quality projects today helps finance and scale the next generation of CDR solutions for tomorrow.

CORSIA compliance is inevitable, but the complex landscape of limited supply at variable quality presents a clear opportunity. By acting now and investing in long-term offtakes of scarcely available high-quality climate assets, leading airlines can secure CORSIA compliance, accelerate the market for durable CDR, and position themselves as market leaders in sustainability.

Ready to build a high-impact, multi-asset climate portfolio? Speak with the experts at CEEZER on how to navigate CORSIA and deliver on both regulatory requirements and genuine environmental progress.