The global energy system is transitioning. According to data from BloombergNEF, annual investment in renewable energy, energy storage, electrified transport, and high-efficiency heating systems reached $1.1 trillion in 2022. This marked the first time that finance for the energy transition matched global investment in fossil fuels.

At the same time, however, the global power sector also reached an “all-time high” level of greenhouse gas (GHG) emissions in 2022, emitting a whopping 13.2 Gt CO2e (IEA, 2023). This accounted for about 42% of global emissions that year (UNEP, 2022). Such an increase in emissions is partly due to the electrification of the global economy and growing energy consumption in developing countries, increasing our dependence on a still carbon-intensive electricity grid.

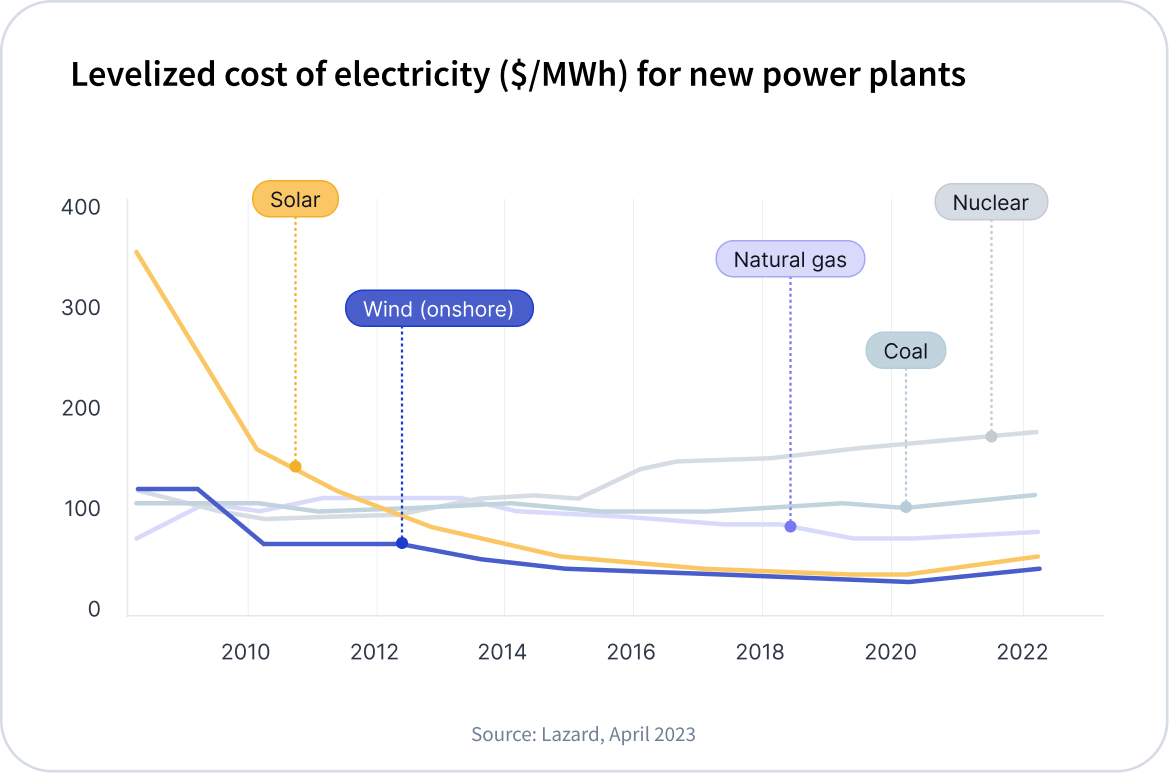

In 2022, wind and solar reached a record 12% of global electricity generation. This significant progress has been largely facilitated by the considerable reduction in the cost of renewables. The graph below captures the levelized cost of electricity over time for various power plant types, reflecting the average net present cost of electricity generation throughout their lifespan. The trajectory for solar energy is particularly remarkable, as its price has become substantially lower than other alternatives over the course of less than a decade.

To meet the climate goals of the Paris Agreement, the share of zero-carbon power in electricity generation should be around 65–92% by 2030, and between 98–100% by 2050 (Monteith and Menon, 2020; IRENA, 2021; Boehm et al., 2022). Fortunately, research shows that this is possible, with Breyer and colleagues (2022) finding that we could achieve a 100% renewable energy system even before 2050.

The voluntary carbon market (VCM) has attempted to accelerate the global adoption of renewables over the past two decades. Indeed, it has funneled significant amounts of finance toward the deployment of wind, solar, and hydropower plants. However, many renewable energy carbon credit projects (particularly hydropower and onshore wind) have been subject to widespread criticism due to their questionable additionality assurances (Haya and Parekh, 2011). In other words, market and technological developments have led to a large share of these projects being economically viable without the added incentive of carbon credit revenue.

This article aims to shine a light on the role that the VCM has played in the energy transition, addressing some methodological limitations associated with renewable energy projects. We will briefly guide the reader through the current renewable energy carbon credit landscape, and provide criteria that can help identify projects that still require finance through the VCM.

How the VCM came into play

Towards the start of the 21st century, the deployment and integration of renewable energy technologies around the world faced a multitude of financial, economic, political, and technical barriers (Sterk et al., 2007). Even when the lifetime costs of renewable energy technologies appear to be cheaper than fossil fuels, risks associated with upfront investment must be addressed to effectively scale up renewable energy technologies.

The Clean Development Mechanism (CDM) has been the main program incentivizing the deployment of renewable energy infrastructure in developing countries (Wissner et al., 2009). This mechanism allowed developed countries to meet part of their emissions reduction commitments under the Kyoto Protocol by purchasing carbon credits from CDM projects in developing countries. Many of the guiding principles and methodologies used by carbon-crediting programs in the VCM today can be traced back to the workings of this mechanism. The CDM aimed to alleviate some of the aforementioned financial barriers by making renewable energy projects more profitable, and thus help procure upfront financing.

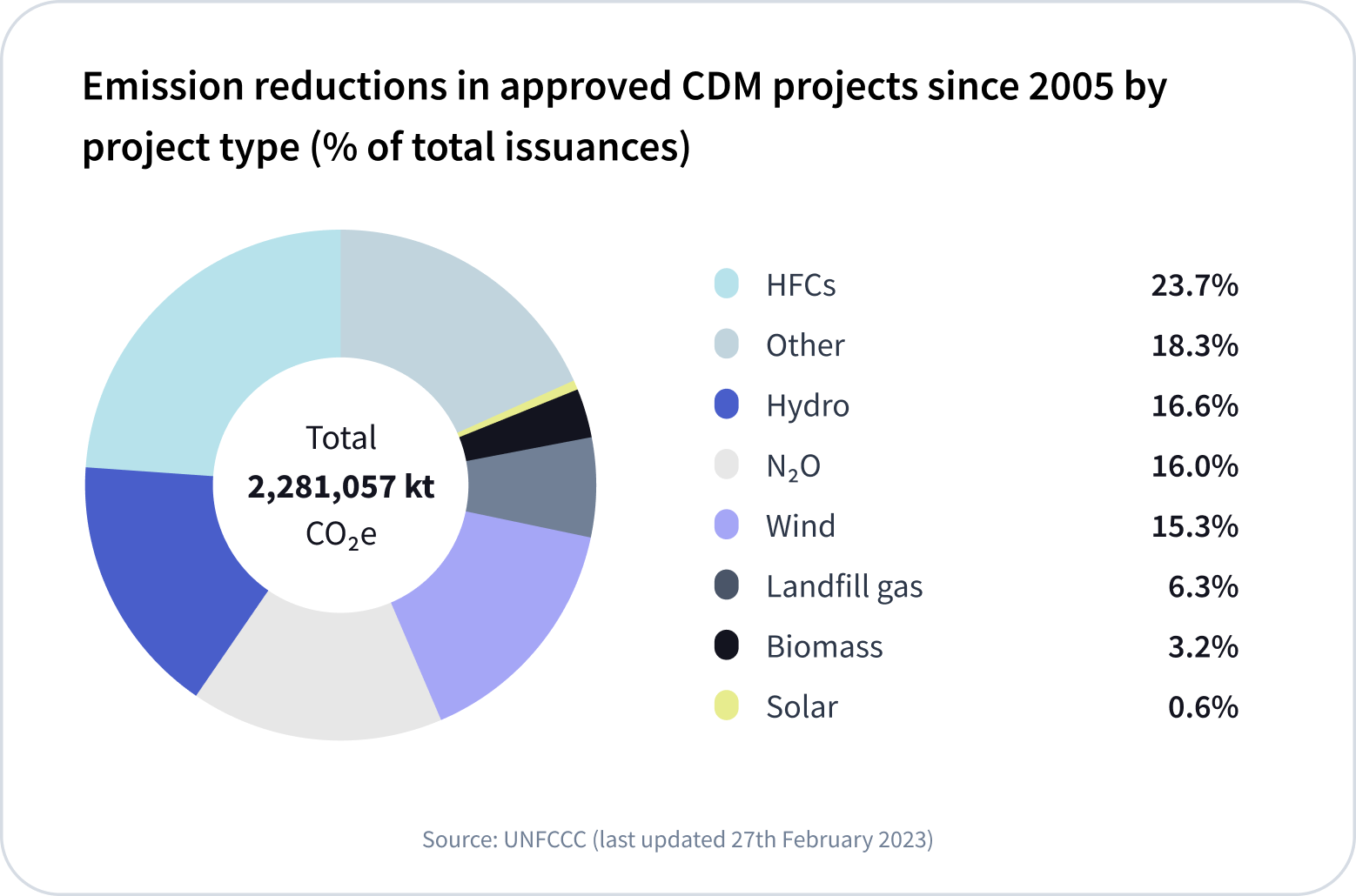

The principle for renewable energy projects is simple: the energy generated by a renewable energy project avoids the GHG emissions that would have otherwise been emitted from burning fossil fuels to generate electricity. The net emissions difference between the project’s scenario and its counterfactual baseline is calculated, and a corresponding number of carbon credits is issued. Therefore, projects in places with more carbon-intensive electricity grids will generate more credits per MWh. Since 2005, CDM projects in developing countries have been generating carbon credits following this principle. As shown below, the bulk of the renewable energy projects under the CDM concerned onshore wind energy and hydropower, whereas solar only accounted for a very minor share.

By the end of 2014, the CDM had supported over $90 billion of renewable energy investments in developing countries. This amounted to approximately 13% of the total renewable energy investments in LDCs at the time (Kossoy et al., 2015).

After 2014, the number of registered projects decreased sharply, and the CDM has been slowly fading out since. In 2020, the Paris Agreement replaced the Kyoto Protocol and, as a result, the CDM no longer accepted applications. However, some established projects that were instituted before the protocol's expiration are still ongoing. It is also worth noting that CDM projects can transition to Gold Standard. Additionally, registries such as Gold Standard and Verra still use several CDM methodologies.

How testing for additionality works

What effect has carbon finance had on individual renewable energy projects? What has been its actual contribution to scaling up renewable energy infrastructure? Before examining the evidence we must first review the concept of “additionality” and the different ways we can test for it.

Fundamentally, additionality evaluates whether a project’s climate impact would have occurred in a business-as-usual scenario. When calculating a renewable energy project’s additionality, the assessment can generally be subdivided into the following three elements:

- Financial additionality: Determines whether the project would have been financially viable without receiving revenues from the VCM.

- Policy & regulatory barriers: Examines whether a project activity is legally required, and assesses the existence of subsidies or other types of support for renewable energy infrastructure.

- Common practice: Analyzes how common renewable energy projects with similar characteristics are in the project’s location and their association with carbon revenues.

In hindsight, renewable energy projects under the CDM have too often failed additionality tests

Additionality was originally assured by the CDM using an “investment tool”. This tool attempts to demonstrate that a prospective project is either not financially viable without the CDM (using investment analysis) or that there is at least one barrier preventing the proposed project in a business-as-usual scenario (using barrier analysis). This tool can be rigorous if it is supported by robust and credible data. However, it is often undermined by the use of unreliable benchmarks that unrealistically deem most projects additional. (Probst et al., 2021)

There is plenty of evidence suggesting that most renewable energy projects surpassed the minimum hurdle rate of return before accessing VCM finance. In other words, suggesting that the project was an attractive investment opportunity even without the revenue from carbon credit sales. According to a study published by the Öko Institut in 2016, most renewable energy projects that operated under the CDM between 2013 – 2020 did not provide real, measurable, and additional emission reductions.

These findings have been corroborated by other similar studies. For instance, Chinese wind projects supported through the CDM were found to be just as viable as those outside of the program (Chan & Huenteler, 2015). Another study found that most Indian wind farms financed through the sale of carbon credits would likely have been built anyway (Calel et al., 2021). The verdict on large-scale hydropower is even more damning, with Haya and Parekh (2011) concluding that these projects should be completely excluded from the CDM because they are unlikely to be ever additional. Finally, one of the authors went a step further asserting that the CDM is “blindly subsidizing the destruction of rivers, while the dams it supports are helping destroy the environmental integrity of the CDM” (Haya, 2012).

Other overcrediting risks: Leakage and baseline updates

With the Paris Agreement replacing the Kyoto Protocol in 2020, the CDM is no longer accepting new applications. Despite this, the program’s impact is still evident as many of these older carbon credits remain available for sale, and various aspects of carbon-crediting programs like Gold Standard and Verra are underpinned by the same principles. Recent renewable energy projects continue to use the approaches of the CDM toward baseline and additionality assessment as blueprints. Yet, their project design is often modified to ensure more rigorous environmental and social standards in an attempt to address some of the CDM's shortcomings.

Interestingly enough, almost half of all renewable energy projects under Gold Standard and Verra share the same methodology (ACM0002), followed by 25% of projects using AMD-I.D. This adds to the aforementioned questionable project additionality assurances provided by standardized carbon credit methodologies. Neither ACM0002 nor AMD-I.D. differentiates between photovoltaic, hydro, tidal/wave, geothermal, and renewable biomass projects. Treating such distinct renewable energy projects the same way inevitably undermines the granularity with which one can assess a project's quality.

Additional issues with renewable energy project methodologies can be exemplified through leakage assessment and baseline scenario calculations. Firstly, following the methodology ACM0002 (used by ~51% of all certified renewable energy projects under Verra and Gold Standard), “emissions potentially arising due to activities such as power plant construction and upstream emissions from fossil fuel use (e.g., extraction, processing, transport, etc.) are neglected.” (CDM, 2022). Considering the large quantities of embedded emissions in the construction of renewable energy infrastructure, neglecting this can result in vast net emissions miscalculations (Lesk et al., 2022).

It is also important to mention that the carbon intensity of the electricity grid is likely to decrease throughout the project’s crediting period. However, standard guidelines and methodologies determine the grid emissions factor ex-ante, only revising this upon the renewal of the crediting period. As a result, renewable energy projects sometimes run on outdated baseline scenarios, leading to an overestimation of avoided emissions.

Market overview: carbon credits from renewable energy projects

The current renewable energy carbon credit market is large, accounting for over two gigatons of avoided emissions annually. As of April 2023, CEEZER has visibility on over 2,652 renewable energy projects (generating almost 300 million carbon credits) from leading standards, which account for around 40% of all projects (25% of all credits) in the VCM.

These renewable energy projects come from two carbon-crediting programs only: the majority are Verra-certified (55% of projects and 66% of reduced emissions), whereas the remainder operates under Gold Standard (45% of projects and 34% of reduced emissions). As shown below, three countries have accounted for almost three-quarters of all projects: India, China, and Turkey.

.png)

The approach of carbon-crediting programs to renewable energy projects in 2023

Renewable energy projects have seen their cost of development decrease over the past decade. In particular, solar and wind energy have become more economical than conventional, carbon-emitting energy sources in many countries.

The two main US voluntary market registries – Climate Action Reserve (CAR) and American Carbon Registry (ACR) – excluded wind and solar projects altogether from the start. Since 2020, the two biggest standards – Verra's VCS and the Gold Standard – also no longer accept newly registered renewable energy projects except for those in the 46 Least Developed Countries (LDCs). This exclusion was driven by the increased affordability and consequent lack of financial additionality of renewable energy projects. Many existing projects will still issue carbon credits in the next few years though, as renewable energy projects typically have ten-year crediting periods.

The exclusion of most new renewable energy projects under Gold Standard and Verra meant that some project owners – particularly in countries such as India, Turkey, or China – have been seeking alternative finance options. Some renewable energy producers that previously generated revenue through sales of carbon credits reportedly moved to the system of International Renewable Energy Certificates (I-RECs) instead. Here, proof of financial additionality is not necessary.

Various old and new projects have also found refuge under the Global Carbon Council (GCC), whose acceptance of renewable energy projects from non-LDC countries made it the new go-to standard.

The Qatar-based GCC is a carbon crediting program that has been operational since 2019 and is endorsed by ICROA. The GCC has been the main source of carbon credits that Qataris have bought for the FIFA World Cup’s questionable carbon neutrality claim. Last year, the GCC stated that over 1,450 emission reduction projects from 40 countries have been submitted for approval. These projects could issue up to 2 billion credits over the next 10 years, but as of March 2023, only 18 projects are approved and listed on the registry.

Despite being one of the most apparent non-additional activities in the VCM, these subpar credits are still considered eligible under CORSIA’s standards. The latest version of its methodology (GCCM001 V3) removed the standardized approach of using a “positive list”, where project activities were deemed automatically additional for certain host countries. Nevertheless, as opposed to VCS and the Gold Standard – which restrict support for renewable energy projects to LDCs – GCC’s approach remains to be lenient.

Financing renewable energy projects in LDCs

Renewable energy projects can still be considered additional in the LDC context due to high mitigation costs and low technical capacity. LDCs often lack the fiscal budgets to upgrade and extend existing infrastructure. While these governments could technically pass on the costs of building such power capacity and infrastructure to their consumers, it is unlikely that consumers will be able to afford this through their electricity bills. Therefore, in such cases carbon credits can work as a useful financial tool for the deployment of renewable energy infrastructure, decreasing the carbon intensity of the electricity grid and supplying access to electricity to thousands of individuals.

Without sufficient stimulus, LDCs may miss out on the opportunity to leapfrog to renewable energy and new, climate-resilient technologies from an early stage, jeopardizing the environmental, social, and economic benefits of such transition. At COP27, the US unveiled the Energy Transition Accelerator, a carbon credit scheme that would fund renewable energy projects in developing countries. It seeks to leverage the growing demand for high-quality carbon credits to scale up finance to speed the deployment of clean power and retirement of fossil fuel assets in developing countries. While the details of the framework are currently being fleshed-out, it has already raised concerns that the credits may support renewable projects that do not require funding.

Financing the early phase-out of coal plants

In order to put the world on a credible pathway consistent with the 1.5 °C goal, the global capacity of renewables needs to triple between 2022 and 2030, reaching around 1,200 GW annually (IEA, April 2023). However, it is not only about adding new capacity but also phasing out existing coal power plants earlier than their historic average operating lifespan.

Between 200,000 – 550,000 annual deaths have been attributed to coal-fired electricity in China, India, the USA, and Europe. Citing these numbers, Gold Standard proposed a new methodology concept in March 2023, to credit the early phaseout of coal-fired power plants and their replacement with renewables.

In its announcement, Gold Standard refers to the need for robust safeguarding and pairing with renewable energy replacement to avoid leakage. This methodology is designed to be applicable for carbon crediting but also explicitly is flexible to other financing mechanisms – such as a ‘just transition bond’. In terms of additionality testing, the concept methodology notes that UNFCCC-approved CDM Tools may be used. However, further options will be explored during the full methodology development.

Recommendations for buyers

Since the number of purchased carbon credits is typically equal to the quantity of emitted tons of the company’s footprint (“ton for ton”), many companies are inclined to choose credits predominantly based on price. As renewable energy is a project type that generally offers a low price point, it is often included in the mix to reduce the average price per tCO2e of a portfolio to compensate for emissions.

At CEEZER, we believe that investing in diverse portfolios can significantly reduce risks and increase the climate impact of carbon credit investments. By including inexpensive renewable energy credits in their portfolio, buyers can diversify their climate impact, partially investing in expensive, long-term technological removal projects as well.

However, the possible inclusion of renewable energy projects is to be taken with the utmost caution. As renewable energy technologies have developed and become more cost-efficient, it needs to be acknowledged that this may come with high non-additionality of over-crediting risks. It is therefore essential for buyers to recognize how to differentiate between projects that are likely to be additional, and those that are not.

For this project type, we advise keeping the following in mind:

- Avoid purchasing CDM credits, and always stick to recent vintages.

- Small-scale renewable energy projects in rural areas are often associated with lower risks than their larger counterparts.

- Opting for carbon credits from renewable energy projects in developing regions that lack financial or technological resources can provide better assurance of additionality.

- Projects situated in LDCs also tend to provide more benefits beyond carbon, such as job creation and economic stimulation within the community.

CEEZER can help to guide the murky waters of renewable energy carbon credits and distinguish the good from the bad. With our expertise, we are able to identify and curate high-quality projects to form impactful portfolios. Moreover, thanks to our close partnerships with reputable project developers, we reduce opacity in the transaction process, and by conducting rigorous screening, we provide greater project additionality assurances. Please get in touch or book a demo today to learn more.