2025 has been the year buyers have taken a long-term, quality-forward approach to carbon investments, looking at the year-to-date market data. In Q3, this trend continued as buyers drove growth in both value and volume, with a focus on value driven by an increased investment in durable removals.

The data paints a picture of an increasingly sophisticated buyer profile and overall maturation of the VCM heading into the last quarter of 2025.

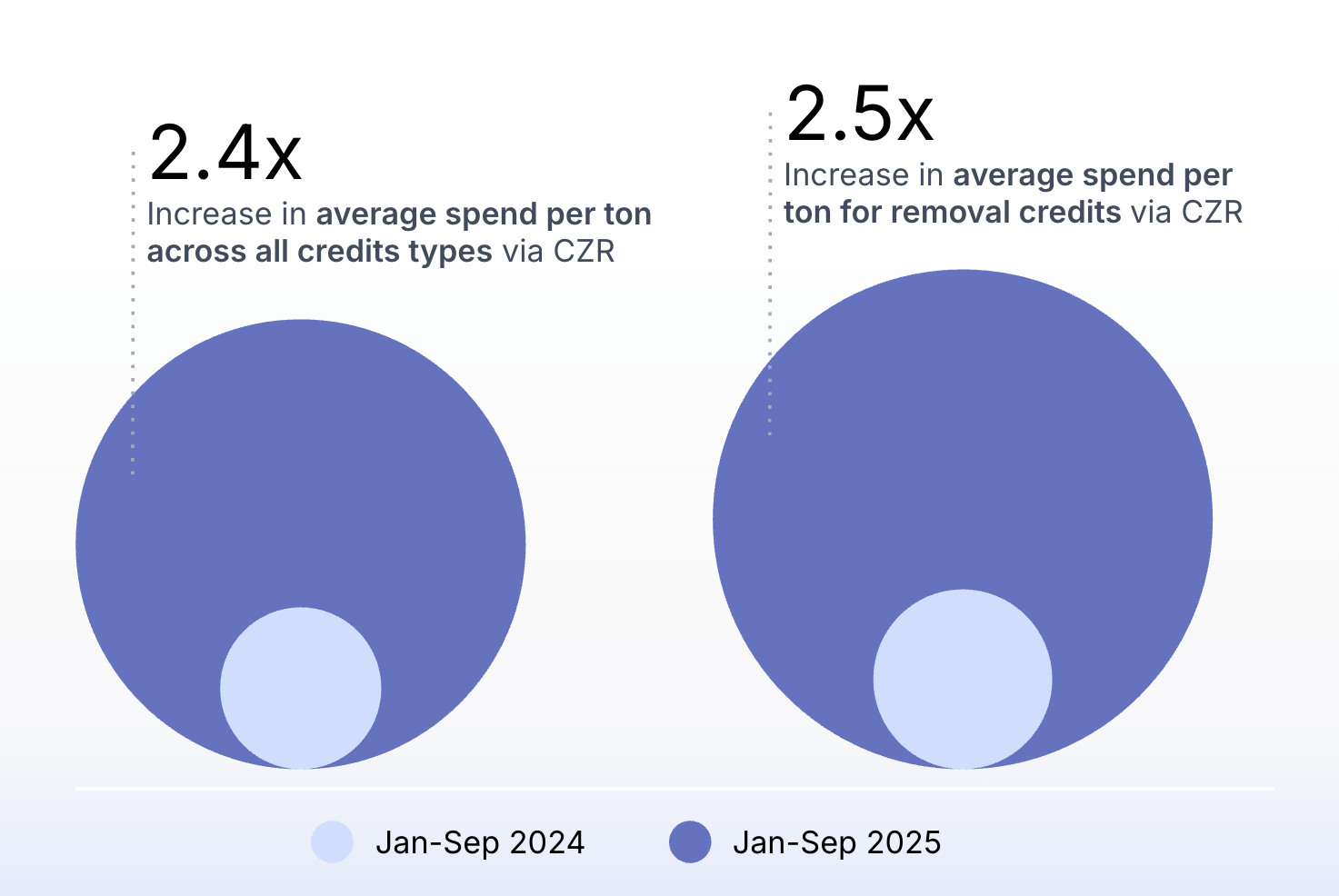

Carbon credit value continues to outpace volume

CEEZER buyers are investing in higher-quality credits and projects, with a surge in removal spending driven by a 35% increase in the share of durable CDR credits within all removal transactions. Average spend per ton across all credit types increased by a factor 2.4x compared to the same period in 2024. For removal specifically, the increase was slightly higher at 2.5x. (Source: CEEZER data).

Retirement volume and value continue to climb in Q3 2025, with value outpacing volume as the market continues shifting towards higher-quality credits. The total value of retired credits increased 22% compared to the same period in the previous year, while the volume only rose 10%. This shows that while the market is growing, buyers are increasingly purchasing higher-priced carbon credits for direct retirement. (Source: CEEZER data, AlliedOffsets data).

Investment in durable removals continues at record levels

The strong shift toward high-quality carbon removal credits continues, with buyers securing durable removals through long-term offtakes. The removal share of transacted volume in tons rose by 79% so far compared to the same period in 2024, almost doubling. This is also visible in the wider market: CDR sales (mostly structured as forward deals) rose by ~4x to $6.4B. While a majority of these CDR credits have not been delivered, and the payments to projects might be tied to successful project performance, this underlines the increasing movement of buyers to secure durable CDR supply for their net-zero years ahead of time. (Source: CEEZER data, CDR.fyi).

Among CEEZER’s buyers, there is a quickly growing engagement in long-term offtake (LTO) agreements, to lock in access to high-quality credits over time ahead of net zero.

Carbon-credit disclosures continue increasing in Q3

CEEZER’s Greenhushing Index – which tracks the share of anonymous carbon credit retirements – continues to fall in Q3, with only 14% of buyers keeping retirements private. After seeing a peak of private retirements in Q4 2024, buyers have decreased the share of private retirements over the course of 2025, reaching a low of 14% in Q3 2025. (Source: CEEZER data).

Overall market prices continue to increase in Q3 ‘25.

Carbon credit prices continue to increase in Q3 ‘25, driven by an increase in demand for removals and high-quality avoidance credits.The average price for a ton of removal (all types) rose 12% to $28.2. Interestingly, avoidance prices increased slowly after staying relatively flat for most of 2024 and 2025 so far, going up to $4.3 (20% compared to a year ago). One possible explanation is the stronger guidance for credible use of avoidance credits as immediate-impact, short-term complement to future removal investments. With quality standards like ICVCM approving more avoidance methodologies under the Core Carbon Principles, their value is increasingly rediscovered. (Source: AlliedOffsets data, CEEZER data).

Biochar and Mineralization continue to lead

Durable removal project types Biochar and Mineralization represent over 64% of transaction value via CEEZER YTD Sept. ‘25, continuing to lead as the most heavily invested in carbon project types. Between Q2 and Q3 2025, ecosystem restoration credits achieved the largest increase in share of transacted value, driven by a 48% rise in their underlying transaction value. This reflects the increasing sophistication with which net-zero portfolios are built using multiple removal pathways to increase impact and spread risk. (Source: CEEZER data).

CEEZER's most trending project types by transaction value are Biochar, Mineralization, Ecosystem Restoration, and Fugitives.

Energy continues to retire most - while professional services make the removal market

The energy sector continues to lead global retirements while professional services drive removal retirements, accounting for 17% of total retirement value and 22% of volume in 2025 so far.

In contrast, professional services represented 3% of global retirement value ($28M) and 2% of volume (3Mt) when looking at the overall market. However, this sector is the single biggest driver for carbon removal demand. So far in 2025, it contributed to 26% of carbon removal retirement value. (Source: CEEZER data, AlliedOffsets data).

If you’d like to discuss this data, your carbon strategy, or how to build a diversified, high-quality portfolio with CEEZER, contact us today.