.webp)

.webp)

The newly adopted European Sustainability Reporting Standards (ESRS) holds profound implications for businesses operating within the European Union (EU), under the scope of the EU Corporate Sustainability Reporting Directive (CSRD). This reporting requirement will become effective from 1 January 2024.

So, what new reporting requirements have been introduced, how will they impact companies purchasing carbon credits, and how can CEEZER support?

The CSRD significantly expands on existing rules on non-financial reporting.

Building upon the Non-Financial Reporting Directive (NFRD), the CSRD will significantly increase the number of companies required to disclose sustainability information. The CSRD entered into force in 2023, and makes it mandatory for all large companies operating in the EU to report on their environmental impact from 2024 onwards.

To ensure affected companies disclose relevant, comparable, and reliable information on all material sustainability-related topics, the CSRD requires entities within its scope to apply so-called European Sustainability Reporting Standards (ESRS).

On 31 July 2023, the European Commission adopted the final version of the twelve distinct ESRSs. The ESRS delegated regulation has been submitted to the European Parliament and to the Council for scrutiny. If accepted, the regulation enters into force after the publication in the official journal of the EU.

The ESRS has three categories of standards:

- 1 standard on general principles for sustainability reporting (ESRS 1)

- 1 standard on overarching disclosure requirements (ESRS 2)

- 10 topical ESG standards, each with specific disclosure requirements (E1-E5, S1-S4, G1-G2)

There’s much to unpack in these documents. This article focuses on the first of the environmental standards, ESRS E1 Climate Change, which includes specific requirements around greenhouse gas emissions, net-zero targets, climate-related claims, and carbon credits.

Reporting requirements regarding carbon credits

The key requirement concerning carbon credit portfolios is found in “ESRS E1-7 – GHG removals and GHG mitigation projects financed through carbon credits.” Companies under the scope of the CSRD will have to disclose their emissions separately from carbon credits purchased, without aggregating the two. In addition, any greenhouse gas (GHG) removals and storage from a company’s own operations and its upstream and downstream value chain (i.e. insetting) must be reported too.

1. Insetting efforts (within the value chain)

In addition to their GHG emission inventories (Scope 1, 2, and 3 emissions), companies must provide transparency on how and to what extent they either enhance natural carbon sinks or apply technical solutions to remove GHGs from the atmosphere in their own operations and upstream and downstream value chain. This is often referred to as insetting.

The ESRS requires these removals to be differentiated by removal and storage type. In practice, that means reporting whether it is biogenic (e.g., afforestation, soil carbon), technological (e.g., direct air capture), or hybrid (e.g., bioenergy with carbon capture and storage). If applicable, technological details about the removal, the type of storage, and the transport of removed GHGs need to be indicated. Here, it also must be explained how the risk of non-permanence is managed, including determining and monitoring leakage and reversal events, as appropriate.

2. Carbon credit portfolios (beyond the value chain)

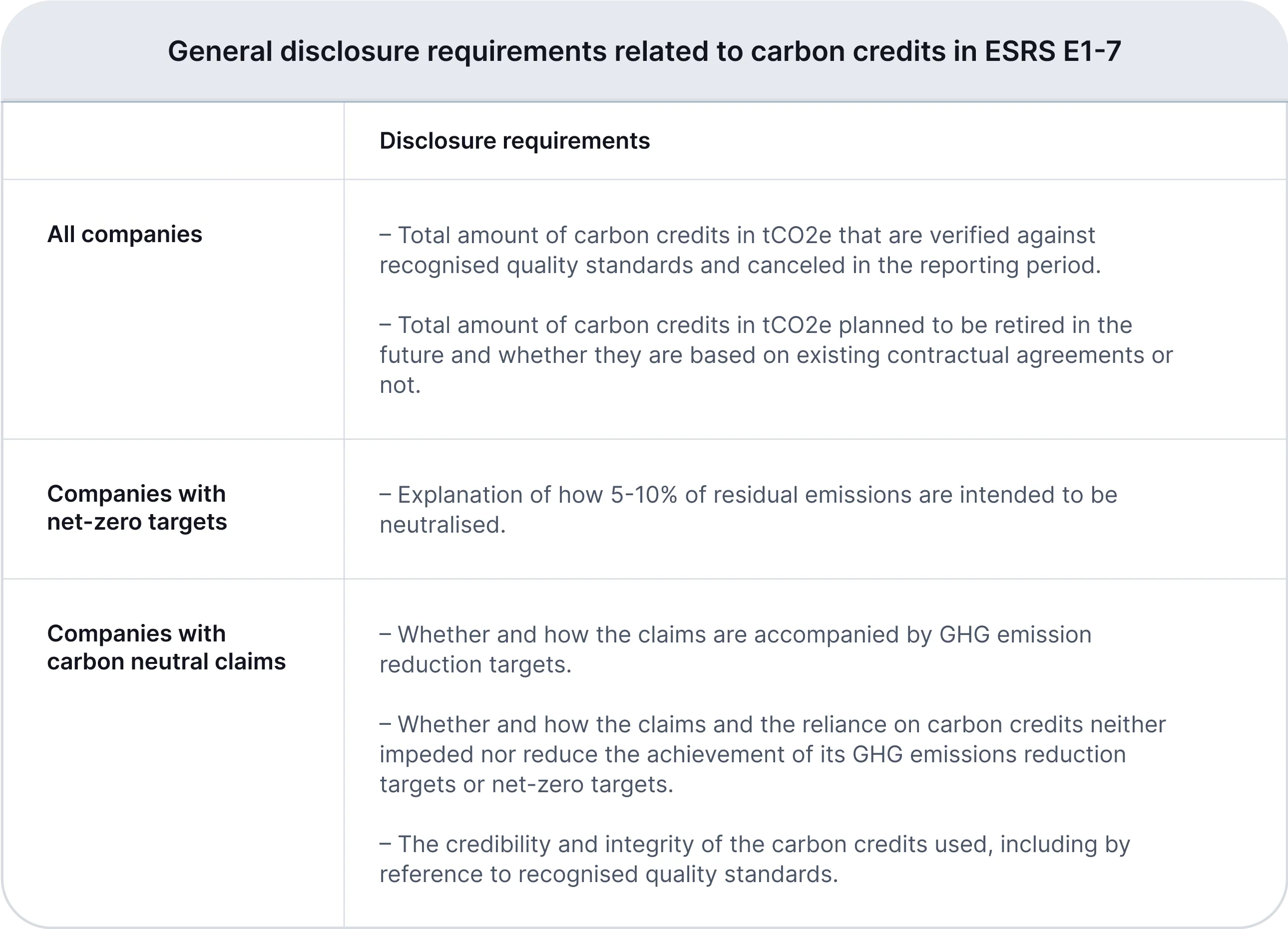

The ESRS recognizes that financing carbon avoidance or removal projects outside the company’s value chain through purchasing carbon credits that fulfill high-quality standards can be a useful contribution towards mitigating climate change. The objective of the standard is to provide stakeholders with an understanding of the extent and quality of carbon credits a company purchased (or intends to purchase) from voluntary carbon market (VCM). As shown in the table below, the requirements differ depending on whether and what climate-related target/claim is made.

When disclosing the information on carbon credits retired in the respective reporting year, all companies shall disclose the following breakdown of the carbon credits:

- Share (%) of reduction projects and removal projects

- For carbon credits from removal projects: an explanation whether they are concern nature-based or engineered removal

- Share (%) for each recognized quality standard

- Share (%) issued from projects in the EU

- Share (%) that qualifies as a corresponding adjustment under Article 6 of the Paris Agreement

When reporting on carbon credits intended for retirement in the future, companies only seem to need to specify the quantity and indicate whether they are derived from existing contractual agreements.

Some of the disclosure requirements need further clarification, such as the definition of “recognized quality standards”. Especially for companies with net zero targets, it is not clear how companies should report on the ”credibility and integrity of the carbon credits used”. It’s also uncertain how CSRD interacts with the upcoming EU’s Carbon Removal Certification Framework (CRCF) and the Green Claims Directive.

How CEEZER helps preparing your business for the carbon credit part of CSRD

The implications of the CSRD for business are material. Companies should act today to get ahead of regulations to ensure compliance and stay competitive. As the enforcement date of the CSRD is looming, it’s crucial for companies to start preparing for this new directive. Especially for companies making public climate-related claims, having the in-depth data on your carbon credit portfolio will be important to meet reporting requirements.

By starting the data collection process early, and working with a carbon credit solution provider like CEEZER, business can meet these new requirements when the time comes.

CEEZER allows companies to generate audit-ready reports from your carbon credit portfolio, and share portfolio impact metrics with key stakeholders. This also applies to credits purchased outside of CEEZER, where credit fundamentals will be mapped automatically to ensure a holistic portfolio content view, including:

- Classification of projects into different types and technologies, clearly distinguishing between nature-based and engineered removal initiatives with indication of permanence using the Oxford Category classification.

- Respective quality standard that issued the credit (ICROA-endorsed or new registries), and its current verification status.

- Geographical locations of projects with a clear split on EU-issued credits.

- Applicability of corresponding adjustments to a project (or expected corresponding adjustment) under Article 6 of the Paris Agreement.

- Data substantiating the credibility and integrity of the utilized carbon credits.

Hence, managing your portfolio on CEEZER comes with built-in reporting in compliance with CSRD requirements, based on rigorous and science-based analysis.

Who is affected?

All companies covered by the CSRD will be required to align their sustainability and ESG reports according to the ESRS. The number of affected companies is is estimated at 50,000.

However, the European Commission has decided that there will be a gradual introduction of specific reporting requirements through phasing-in reliefs. Companies will have to start reporting under ESRS according to the following timetable:

.webp)

For more exact information on which companies will need to implement these standards and when, see this Q&A article from the European Commission (31st of July 2023).

Mandatory is the new voluntary. Get ready

Currently, voluntary disclosure is still the norm. However, upcoming regulations regarding climate disclosure will greatly affect companies purchasing carbon credits soon, including frameworks like CDP, ISSB, and SEC Climate Disclosure Rule in addition to CSRD.

We're moving into a time where sustainability reporting is as crucial as financial disclosures. Despite some remaining uncertainties about the exact implementation of the various disclosure requirements, leading enterprises are proactively organizing their data to comply with new regulations.

Be prepared. Change is on the horizon, and those who get ready now will lead the way tomorrow.

With CEEZER, you can easily build, manage, and report on an impactful portfolio aligned with your climate action goals. Leveraging the data-rich view on carbon portfolios is the consequence - and allows to fulfill reporting requirements on carbon credits “out of the box”. To learn more about about upcoming reporting requirements or our platform, please get in touch or book a demo today.